Comparison: Reverse Mortgages vs. Home Equity Investments — What They Are and Which Works Better?

I meet with many older homeowners who have substantial home equity, little or no other assets, and very limited income. The goal of many of these clients is to age in place for as long as possible, and the main question for these clients is how best to tap into their home equity to pay for in-home care, without

having to make monthly payments. While paying for in-home care is typically the main motivator to tap into home equity, sometimes there are different financial goals driving the need to tap into home equity, such as the ability to pay fees for an assisted living facility or other alternative housing, or even legal or other necessary fees, either pending the sale of a home or without being forced to sell the home.

Historically, the two product categories most commonly mentioned

were HELOCs (which don't work for this type of client because they don't have sufficient income to make monthly payments), and reverse mortgages (the most common called a HECM, which stand for Home Equity Conversion Mortgage). But in the last decade or so, a new method of tapping into home equity has started growing in popularity but is still a very new concept in the financial industry — the Home Equity Investment (HEI).

An HEI is in some ways

similar to a HECM reverse mortgage, but they function very differently and are not interchangeable — especially when the goal is funding long-term in-home care.

This article focuses on traditional HECM reverse mortgages v. the newer Home Equity Investment (HEI) products, because in elder law practice those are the two products that realistically apply when a client cannot make monthly payments.

Before comparing them, it is essential to define each

product clearly.

Defining the Products

HELOCs (Home Equity Lines of Credit).

A HELOC is a revolving line of credit secured by the home. It requires sufficient income and ongoing monthly payments. For low-income seniors, HELOCs are usually unavailable or inappropriate, which is why they are not the focus here.

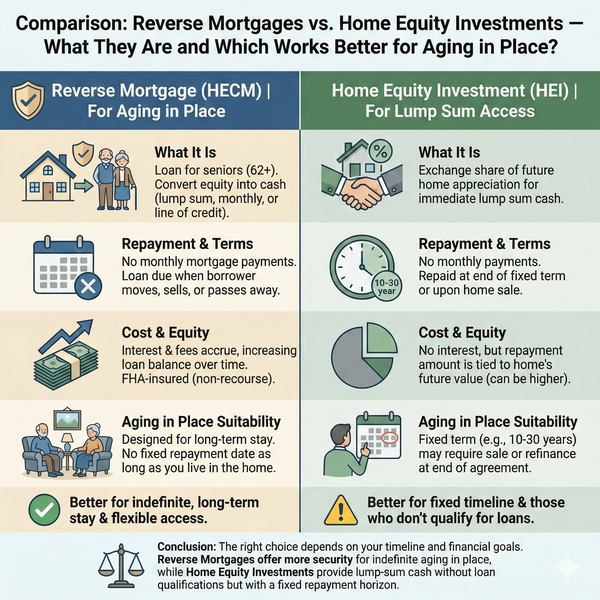

HECM Reverse Mortgages.

A HECM (Home Equity Conversion Mortgage) is a federally

insured reverse mortgage overseen by HUD. It allows homeowners who still live in their home and are at least age 62 to access home equity without monthly payments. Funds can be taken as a lump sum, a line of credit that grows over time, monthly payments, or a combination. The loan becomes due only when the borrower permanently leaves the home, dies, or fails to meet basic obligations such as paying property taxes and insurance. The requirement that the homeowner still be living

in the home is a critical element for HECMs, and a critical distinction between HECMs and HEIs.

Home Equity Investments

A Home Equity Investment (HEI) — often called home equity contracts or shared-equity agreements — is a relatively new financial product. The homeowner receives a lump sum today. In exchange, the HEI provider receives a contractual right to a percentage of the home’s value in the future, typically upon sale, refinance, or at

a stated maturity date. There are no monthly payments, but the future cost is uncertain and tied to home value at exit. Of vital importance for some families . . . there is generally no requirement that the homeowner still be living in the home to get an HEI, so long as a family member is living in the home, which is a critical distinction between some HEIs (which do not require the homeowner to live in the home) and HECMs (which, as explained above, always require the homeowner to be living in

the home and continue to live in the home).

Major national providers include Hometap, Point, Unlock, Unison, Aspire, and Splitero, though more and more national and regional players have entered the marked in the past several years. We do not endorse any specific

product.

The financial website SuperMoney has a good resource for comparing the different HEI providers. SuperMoney is an established company with a public history of operating as a finance comparison marketplace. User reviews on third-party platforms such as Trustpilot generally rate it positively for its review and comparison tools. However,

SuperMoney earns revenue through affiliate referral fees, sponsored or featured placement, and lead generation, which means its comparisons, though helpful, are perhaps not fully independent and unbiased.

The most independent, authoritative, and unbiased overview available is the Consumer Financial Protection Bureau’s Issue Spotlight on the home equity investment market. Anyone considering an HEI should read this CFPB report first, as it explains how these products work and compares them to HELOCs.

What neither the CFPB report nor SuperMoney do is directly compare HEIs to reverse mortgages in the context of a borrower looking to tap into home equity mainly for the purpose of paying for in-home care in order to age in place, which is

the gap this article fills.

Why this Comparison Matters in Elder Law

In an elder law context, the primary reason someone accesses home equity is not lifestyle spending. It is to pay for in-home care so they can remain safely in their home as they age. That purpose highlights differences between HECMs and HEIs that are not obvious in marketing materials.

Key questions become:

• Will the product still work if your care needs last many years?

• Is

there a forced end date unrelated to health or housing needs?

• Can funding adapt as care costs increase over time?

How Quickly Funds are Available

HECMs

• Typical timeline is 45 to 75 days, sometimes longer.

• HUD-approved counseling is mandatory.

• Full appraisal and mortgage underwriting are required.

• Funds may be accessed incrementally rather than all at

once.

HEIs

• Typical application-to-funding timeline is approximately 3 to 6 weeks, assuming no title issues.

• Underwriting is lighter than a mortgage.

• Funds are delivered as a single lump sum.

• No counseling requirement.

Speed can matter in a care crisis, which is why many people are drawn to HEIs, but over a multi-year aging-in-place plan, flexibility usually matters more than speed, and

HECMs work out better in this regard.

Contract Duration — the Biggest Difference Between HECMs and HEIs

Every HEI has a mandatory settlement trigger, and virtually all have a maximum contract term. This is not a detail — it is a core risk factor, and it varies by provider. Some HEIs last only a maximum of 10 years; some can go on for 20 or 30 years.

By contrast, a HECM has no fixed term. It ends based on life events, not the passage of

time.

Feature | Hometap | Point | Unison | HECM |

|---|

Monthly Payments | None | None | None | None |

Typical Funding Structure | Lump sum | Lump sum | Lump sum | Lump sum, line of credit, monthly payments |

Maximum Contract Duration | Commonly up to ~10 years | Often 10–30 years, depending on product | Often up to ~30 years | No fixed term |

Required

Settlement | Yes — sale, refinance, or maturity | Yes — sale, refinance, or maturity | Yes — sale, refinance, or maturity | Only upon death, permanent move, or default |

Cost Certainty at Inception | Low | Low | Low | High (regulated formulas) |

Credit Score Generally Needed at Inception | 585 | 500 | 680 | High (regulated formulas) |

Line of Credit Growth | No | No | No | Yes |

Fit for Long-term Care Funding | Limited | Limited | Limited | Strong |

HEI Occupancy and Rental Rules by Major

Providers

A practical question many families ask is this: if Mom has to move out to go to assisted living or to a nursing home, can the contract stay in place if an adult child continues living in the home, or if the home is rented?

Provider marketing often does not highlight this, and it can vary by company and contract. Below is what these providers state publicly.

HEI provider | Must the homeowner continue living in the property after closing? | If the homeowner moves out, can a family member live there to keep the contract in place? | Can the property be rented

during the HEI term? |

|---|

Hometap | Not clearly disclosed in public materials; generally described as originating on owner-occupied primary residences. | Not clearly disclosed publicly; contract language must be reviewed. | Not clearly disclosed

publicly. |

Point | No explicit requirement that the homeowner continue living in the property after closing. | Not expressly stated, but family occupancy is generally compatible if rental use is permitted. | Yes. Point states the home may be rented, but the rental period may

not exceed the term of the Option Purchase Agreement. |

Unlock | No. Unlock states it invests in primary residences, second homes, and rental properties. | Not expressly stated, but family occupancy is generally compatible because rental use is permitted in many cases. | Yes.

Unlock states rental or investment properties may be eligible, though limits may change and restrictions may apply by location. |

Unison | Yes. Unison states its programs are designed for owner-occupied primary residences. | Not clearly disclosed publicly; owner-occupancy requirement suggests move-out may trigger

issues. | Not disclosed publicly as permitted; primary-residence focus suggests rentals are not allowed. |

Aspire | Yes. Aspire states the homeowner must live in the property. | No. Aspire’s stated owner-occupancy requirement does not accommodate family

substitution. | No. Aspire states investment or rental properties are not eligible. |

Splitero | Not always. Splitero states that, in some cases, second homes or investment properties may be eligible. | Not clearly disclosed publicly. | Potentially yes in some cases, because investment properties may be eligible, but details are not clearly disclosed publicly. |

Scenario Analysis Using Real World Elder Law Fact Patterns

All examples assume very low income and no liquid assets other than home equity.

Age 85, Home Worth $900,000, No Mortgage

At this age, the planning

horizon is shorter and more bounded.

HEI Considerations:

• Upfront proceeds are typically a modest percentage of home value.

• A 10-year HEI is not inherently inappropriate at age 85, but hugely problematic if the borrower lives past 95 and is otherwise able to continue to live in the home.

HECM Considerations:

• Principal limits are high at advanced ages.

•

Funds can be staged as care needs increase.

• No maturity risk tied to age 95.

Age 75, Home Worth $800,000, $200,000 Mortgage

This is a more balanced but risk-sensitive scenario.

HEI considerations:

• A significant portion of proceeds may be consumed paying off the existing mortgage.

• Remaining cash for care may be lower than

expected.

• A 10-year term or even 20-year term creates real longevity risk.

HECM considerations:

• Existing mortgage can be paid off within the HECM.

• Remaining availability can fund care over time.

• No forced exit if care needs extend beyond expectations.

Age 65, Home Worth $700,000, $300,000

Mortgage

This is where HEIs are most aggressively marketed — and where risks are often understated.

HEI considerations:

• Younger age means lower upfront proceeds.

• A 10-year HEI is likely a very poor match at 65 due to high probability of outliving the contract, so should probably only consider a 30-year option.

• If shorter than 30 years, rorced settlement may occur

precisely when care needs peak.

HECM considerations:

• Lower initial principal limit, but still substantial.

• Line of credit growth over decades can be significant.

• Designed for long planning horizons.

Medicaid and planning implications

From an elder law perspective:

• HEI lump sums can create countable assets if not handled carefully.

• HEI

contracts can complicate later Medicaid planning due to valuation and equity-interest issues.

• HECMs are well understood by Medicaid agencies and integrate cleanly into established planning strategies when structured properly.

Regulatory Scrutiny

Some HEI companies have been sued by state regulators alleging illegal practices. See, e.g.,

Massachusetts AG sues Hometap, saying company offers illegal home equity investments that really are reverse mortgages

Courts in Several States Expose Deception of Home Equity “Investments”

These developments are important because they highlight that HEIs may not be insulated from lending and consumer protection laws, particularly when courts or regulators look beyond label to substance — which is exactly the analytical lens that elder law practitioners must apply when comparing HEIs to HECMs.

Bottom line

HEIs are legitimate options for seniors looking to

tap into home equity, and they are not universally bad products, but they should always be compared carefully to a reverse mortgage. HEIs are time-limited contracts and reverse mortgages are not, and time often matters enormously in retirement planning.

For seniors whose goal is to fund in-home care over an uncertain and potentially lengthy period, HECM reverse mortgages remain the most durable, flexible, and regulator-tested option available. HEIs may work in narrow,

carefully defined situations, but they are not functional substitutes for reverse mortgages when aging in place is the objective.

Anyone considering an HEI should first understand how these contracts work, read the CFPB Issue Spotlight, and then evaluate whether a product with a built-in clock truly aligns with the realities of longevity and care.